The latest credit card on the scene, the Uber credit card, is about to start taking applications (November 2). It is unusual in a couple of different ways (see 4 Surprising Things about the Uber Credit Card). But, there are some things that I believe credit card issuers could learn from this card that would be beneficial.

What Credit Card Issuers Could Learn from the Newest Credit Card

To recap, here are the key points with the Uber credit card:

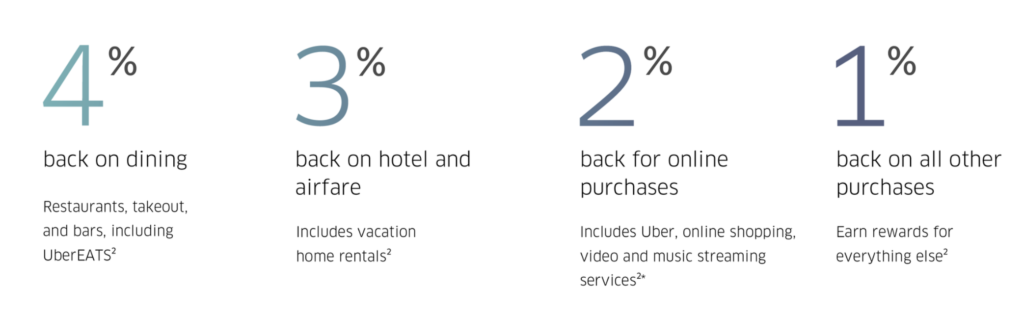

The new Uber credit card’s category bonuses

- 4% back on dining

- 3% back on hotel and airfare (including vacation rentals like AirBnB)

- 2% back on online purchases (not made through third-party wallets like Apple Pay, Samsung Pay, etc)

- $50 credit for net purchases from eligible digital music, video and shopping subscription services after you spend $5,000 or more in total net purchases on your account during each 12-month period

- Up to $600 in cell phone coverage

Remember, this is all on a no-fee card! It is certainly a different kind of offering and there are some things that I think could help both issuers and the customers.

Select Categories on Bonuses

The interesting part with the category bonus is the 4% on dining and 3% on many kinds of travel. For a no-fee card, that is very generous! When I first saw that, I thought about how many people may be pursuaded to move this card to the front of their wallet for those categories, especially all those that are interested in cash back (the Chase Sapphire Reserve offers 3 points per dollar on travel and dining but if you look at it as cashback, the $450 annual fee kills that).

The Amex Business Gold Rewards card offers select categories for 3X earning (up to $100,000 per year)so a chosen category bonus is not unusual. The Chase Freedom and Discover cards offer rotating categories at the 5% amount also. Again, this is a valuable feature but one that is capped.

Special category bonuses could push credit cards to the front of the wallet | Courtesy of Shutterstock

What I Would Like to See

A great feature would be a credit card allowing customers to choose any category for bonus points or cash back. It could be something like a 3X or 4X bonus but with a cap. This would help the credit card issuer but it should be something like a $25,000 or $50,000 in spending cap per year. If it is a single category, that is not too bad since things like office supply stores get 5X earnings up to $50,000 in spending per year and they sell gift cards. 🙂

How This Would Help Issuers

Being able to select a spending category for bonuses would help the card issuer since the customer would be more likely to move that card to the front of their wallet for spending that happens on a regular basis.

Credit card issuers are fighting for that precious place in the wallet and it could help them get that by giving the customer bonus points for the spending they most often have.

Certain Bonuses or Features for Specific, Monthly Bills

The Uber credit card offers cardmembers up to $600 in cellphone insurance coverage – if they put their whole monthly bill for cell phones on the card. This is very smart as smartphones are getting higher in price now than ever and so are the replacement costs. This is of concern to customers so offering this perk in exchange for their monthly cell phone bills is really great.

Cell phone bills for a single person can be between $70 – $100 per month. That translates to approximately $1,100 in guaranteed spending each year.

What I Would Like to See

This is a great idea and one that any other card issuer could easily implement. Of course, credit card companies could offer the same exact thing or target another kind of monthly spending.

Credit card issuers already offer coverage for certain kinds of purchases or protection against price drops, etc. This new feature from the Uber credit card would present an interesting piece of competition on another card.

How This Would Help Issuers

It pretty much goes without saying – requiring a monthly or regular spending on a credit card gives the card issuer guaranteed charges.

Specific Credit for Cumulative Spending

Giving credit for specific kinds of spending can be a big help | Courtesy of Shutterstock

Uber offers a $50 credit for subscription services for spending $5,000 in a cardmember year. That $5,000 spending can be on anything but the $50 credit is for specific purposes.

What I Would Like to See

This is an extra, specific bonus of 1% on spending. It targets the cable cutters who watch a lot of subscription-based services. It does not take from the 1% cash back earning on the day-to-day spending on the card.

It would be great to see a card issuer offer something like this for online shopping or travel companies. If it is a co-branded credit card, it would great to see something like a $100 gift card for an airline or hotel for putting $7,500 – $10,000 on a card in a year. This would certainly help to push consumers to use that card for more spending.

Some cards, specifically hotel cards, have offered bonuses for tiered spending. That is nice but could be considered simply an anniversary bonus since hotel competitor cards do offer anniversary nights with the annual fee and no annual spending.

How This Would Help Issuers

Again, this would push the credit card to a more often used card. By itself, it would not be enough for the bulk of us. But, combined with things like the specific categories and the cumulative spending credit, it would certainly be a great one-two punch against other cards in our wallets.

Takeaway

Will we see a card offer things like this? Hard to say. I would say a couple of years ago “no” but times have changed. Credit card issuers are targeting millennials and shutting down things like card churning and various forms of manufactured spending. Credit card issuers could both push back and reward customers by actually giving something of substance instead of the same old card benefits that we see on most credit cards today.

What would you like to see on the next credit card?