Yesterday, we were greeted with an anticipated new credit card – the Barclays Arrival Premier card. This card had so much potential in what it could have offered and what it could present as value to customers for an ongoing relationship.

Biggest Reason NOT to Apply for the New Barclays Arrival Premier Card

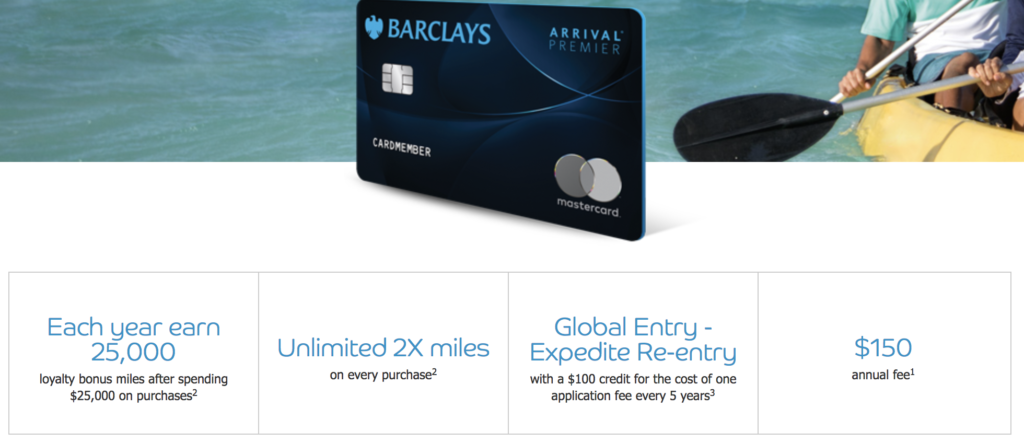

Yet, Barclays really, really missed the boat with this card. Not only do they have largely mediocre airline transfer partners (with JAL being the only truly interesting partner since their only other transfer partner is SPG), but they have no sign-up bonus and the only way to make this card come out ahead of similar cards is by spending $25,000 in a year.

It is laughable that this card was supposed to be entering the “premium” card space. That space is dominated by cards like the Chase Sapphire Reserve and the American Express Platinum cards. Let’s take a look, for a minute, at what the differences are between the Chase Sapphire Reserve and the Barclays Arrival Premier:

Sapphire Reserve vs Arrival Premier

| Card Details | Chase Sapphire Reserve | Barclays Arrival Premier |

|---|---|---|

| Sign-Up Bonus | 50,000 points | 0 points |

| Annual Fee | $450 | $150 |

| Annual Travel Credit | $300 | $0 |

| Transfer Ratio | 1:1 | 1.4:1 | 1.7:1 |

| Point Value for Travel | 1.5 Cents per Point | 1 Cent per Point |

| Transfer Partners | Aer Lingus, British Airways, Flying Blue, Iberia, Korean Air, Singapore Airlines, Southwest, United Airlines, Virgin Atlantic | IHG, Marriott, Ritz-Carlton, Hyatt | Aeromexico, Flying Blue, China Eastern, Etihad, EVA Air, Japan Airlines, Jet Airways, Malaysia Airlines, Qantas |

| Lounge Access | Free Priority Pass with unlimited guests | $27 per visit with membership |

| Global Entry Credit | $100 every 4 years | $100 every 5 years |

| Earning Rate | 3X points on travel and dining, 1X points on all other purchases | 2X points on all purchases |

| Annual Spending Bonuses | N/A | 15K points after spending $15K | 10K additional points after spending $10K more |

| Total Minimum Value in First Year (Spending $25K in a year with $5K being travel and dining) | $1,225 | $700 |

Keep in mind that JAL as a transfer partner does have increased value because of their only other transfer partner being SPG. But, they also lose a few points due to the huge surcharges now charged for Emirates awards.

So, What is the Biggest Reason NOT to Apply?

We have seen time and again – airlines and hotels copy each other with devaluations. They enjoy letting one go first and trial out the changes to see if they will be profitable for the airline or hotel.

This is certainly the case with card issuers as well. None of them want to give more than they have to to retain customers and earn a profit for year-after-year customers.

This new Barclays card will certainly be something that card issuers like Chase, Amex, and Citi will be watching to see how well it is received (or not received) by customers – that is the biggest reason not to apply! We do not want to give these other issuers any excuse to think they could start offering sub-par card offers like this one or downgrade the great cards they already offer

Terrible Transfer Ratios

Amex, Citi, and Chase have given us the norm of 1:1 transfer ratios for most travel partners and is what we have grown used to. I would guess that any one of them would like to devalue those ratios but they know it will be a hard sell.

We know from Barclays themselves that the primary purpose is the 1 cent per point redemption as opposed to the transfers to partners. They look at that more as a way to top off accounts (and who among American cardholders routinely need to top off those accounts???).

The 2X Points Is Somewhat Negated by the Annual Fee

The Barclays Arrival Premier launched with bad transfer ratios – and we cannot say it is okay because of generous 2X earn rates (up to 3X rates if you spend $15K or $25K in a year). The Chase Freedom Unlimited earns 1.5 points per dollar (when matched with a UR earning card, they can be used as UR points) on everything and transfers at 1:1 to all partners. Also, the Amex Business Blue Plus earns 2 points per dollar and transfers at 1:1 as well. Plus, neither card has an annual fee!

Let’s say we spend $25,000 on all 3 cards and want to transfer to an airline partner. Here is how that would convert (while deducting $150 worth of points from the Arrival Premier for the annual fee):

- Amex Business Blue Plus – 50,000 airline miles

- Chase Freedom Unlimited – 37,500 airline miles

- Barclays Arrival Premier – 42,857 airline miles (35,200 JAL miles)

It gets worse if you were to spend $50,000 per year on a card. Here is the comparison between the Amex Business Blue Plus and the Barclays Arrival Premier:

- Amex Business Blue Plus – 100,000 airline miles

- Barclays Arrival Premier – 78,571 airline miles (64,705 JAL miles)

1 Cent Per Point for Travel

This is similar to the previous Arrival + but without the rebate. As a premium card, it falls very short. This is what we get from other issuers of premium cards:

- Chase UR Earning Cards – 1.25 cents per point (1.5 cents per point for the Chase Sapphire Reserve)

- US Bank Altitude Reserve – 1.5 cents per point

- Amex Business Platinum – 30% rebate

- Citi ThankYou Cards – 1.25 cents per point

I am certain that card issuers are looking at the potential of allowing for less value on points when redeemed for travel. As airlines diminish their own miles for such use (recent Southwest devaluation of point values and Delta allowing 1 cent per mile with Pay with Miles), banks would also like to decrease their own value of points. A card like the Barclays Arrival Premier is a bad test case.

No Unique Benefits

Seriously, offering a “premium” card with a $150 annual fee and no unique benefit? That is just insulting to potential customers. Barclays did a nice job of going unique with their Uber card (no annual fee, by the way) and I thought they would do something similar with their Arrival Premier.

Again, dangerous signal to other issuers if they do not package nice benefits in with a high annual fee.

No Sign-Up Bonus

I have to think that this is temporary – why in the world would an issuer think they could get away with a higher annual fee card with no sign-up bonus? Again, this is a dangerous precedent if customers are willing to fork over $150 up front with nothing back in return.

Takeaway

As you can tell, I am seriously not a fan of the Barclays Arrival Premier card in its current state. Maybe if I had affiliate links I would feel different 😉 – just kidding as I do not let those links direct my content.

If anyone starts pushing this card as a good deal for the customer, definitely do not look at that person/site as an expert in this field. Yes, this card has interesting transfer partners but paying a $150 annual fee for the access to those partners is definitely not worth it.

Come on, Barclays. You can do better!

How about you take that nag out back of the barn and put it out of its misery while I go up to the kitchen and call the dog food factory? The less said about any of this ever again the better, far as I can see.

Agreed, spot on

[…] list of properties that cannot be redeemed using the certificate. Barclays has launched their new Arrival Premier Card and is a huge disappointment for almost everyone. The new card still earns 2x miles per dollar spent, but the miles can only be […]

[…] list of properties that cannot be redeemed using the certificate. Barclays has launched their new Arrival Premier Card and is a huge disappointment for almost everyone. The new card still earns 2x miles per dollar spent, but the miles can only be […]

You mention surcharges for Emirates awards, but they’re not a transfer partner for the Barclays product. Etihad is, and they’re the odd airline charging per-sector award charges.