Unless you have someone else paying your tuition, odds are you are one of the many people with student loans. When I graduated pharmacy school I had a nice 6 figure student loan debt and I am sure some of you can relate. I recently received an email from SoFi and JetBlue mentioning refinancing (although I no longer have any student loans) and earning a nice chunk of miles. But, should you refinance your student loans for JetBlue miles?

Should You Refinance Your Student Loans For JetBlue Miles?

Backstory:

When I graduated pharmacy school in 2012, I had about $165,000 in student loan debt. My interest rates ranged from about 6% to 8%. My monthly payments were about $2,000 per month and would have been for the next 10 years. Each time I made a payment, roughly 50% went to interest.

It was quite agonizing to see $1,000 in interest accrue each month and my hard work really not making a dent. Two steps forward, one step back is what it felt like.

I had started looking at refinancing my student loans in an effort to reduce the amount of time and money I would pay on my student loans.

I ended up refinancing with SoFi and all I received from them was a t-shirt (which is by far the softest shirt I own 🙂 ). I would have gladly taken 50,000 JetBlue miles, but my situation/ability for refinancing might be very different from yours.

So back to the scheduled post.

Federal Student Loan Protections:

When we look at credit cards, we like to see what type of benefits we will receive, such as travel protections. Many put travel expenses on a credit card that has some sort of delay or lost baggage coverage.

Why? We want to make sure we are covered in the event something happens.

Federal Loans have extra protections that Private (Refinanced Loans) do not have. These decisions must be taken a little more seriously than worrying if you should put your trip on your Chase Sapphire Reserve or your American Express Platinum.

You have multiple ways for repayment with Federal Student Loans:

- The Standard 10 year plan

- Income Based Repayment

- Extended Payment

- Income Contingent Repayments

- Public Loan Forgiveness

Lost your job or have some other economic hardship, you can:

- Suspend payments on your Federal Loans for up to 3 years.

- Your unsubsidized student loans, will still accrue interest. This will need to be paid back, but you won’t have to worry about it during your economic hardship

- Forbearance allows you to suspend your student loan payments in one year increments for up to 5 years.

Not only do you have protections, but you also have more options for repayment. They aren’t perfect by any means, but having options is always a positive.

The protection you receive in the event of some sort of economical hardship are far better with the Federal Loan Lenders. If you decide to refinance, you are moving your loans from the Federal lender to a private lender. With that move, comes a reduction on protections.

We can relate this to credit cards right? The Chase Sapphire Reserve is like Federal Loans, and the American Express Platinum is refinancing your loans.

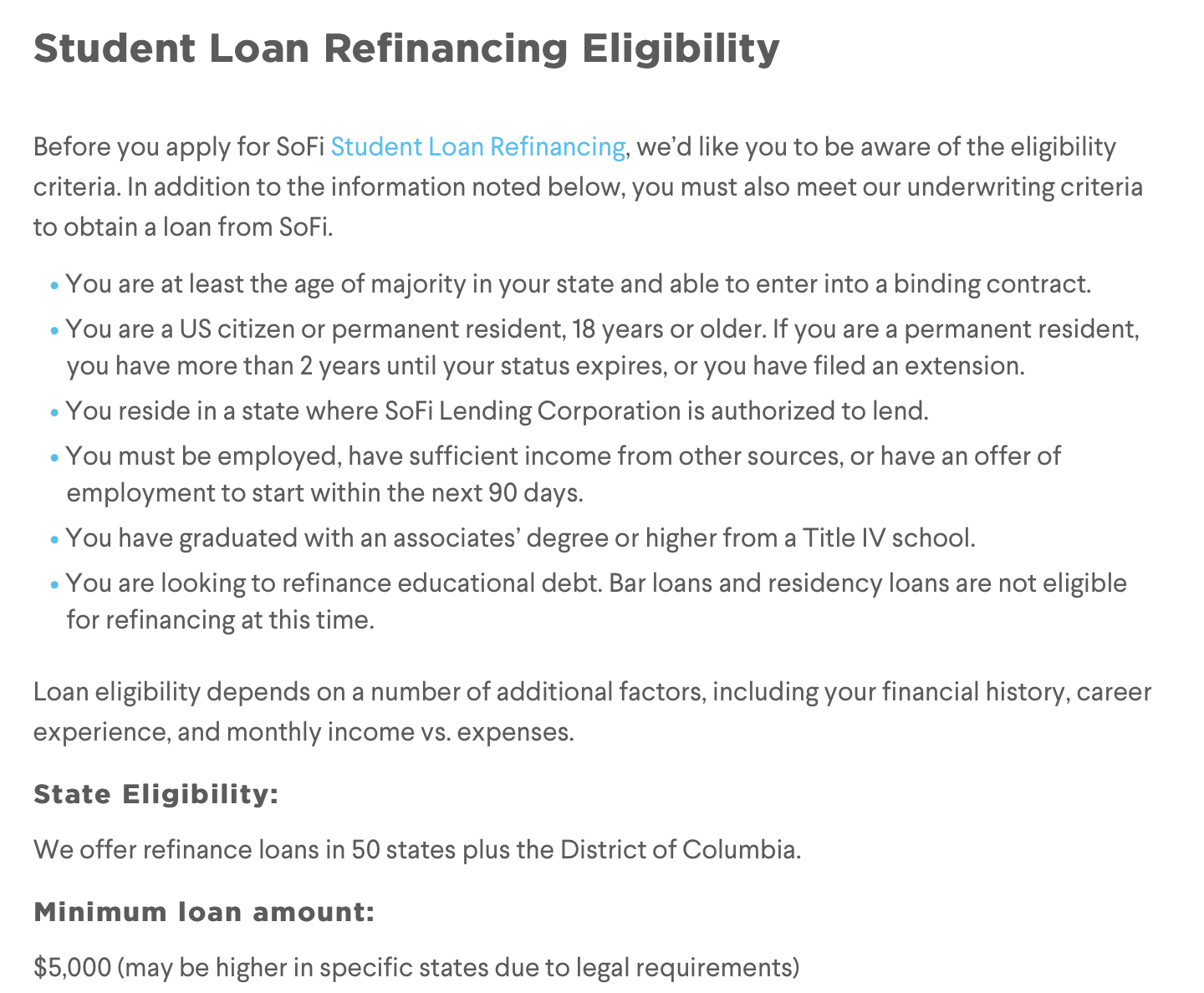

SoFi Eligibility:

SoFi does have criteria you must meet before you can refinance your student loans.

I am not sure why it says you need to live in a state where SoFi is authorized to lend, then they say they offer loans in all 50 states and Washington DC.

You must have graduated with a degree from a Title IV school. A Title IV school processes U.S. federal student aid, such as Stafford loans.

A few types of loans are excluded as well.

SoFi’s Protections:

When compared to the Federal Student Loan protections, SoFi’s protections are a bit underwhelming. Then again, other companies are just as underwhelming.

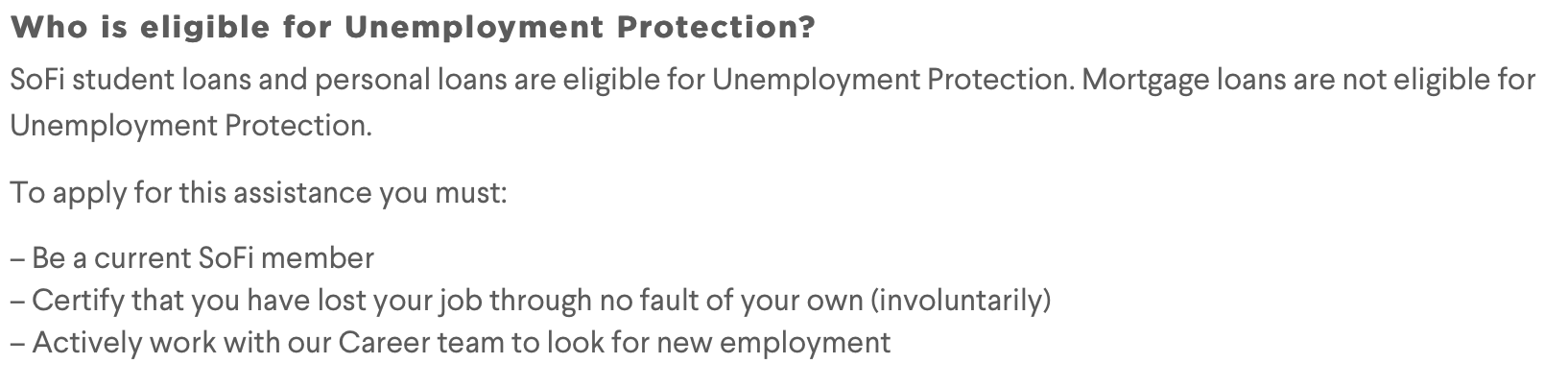

If you were to lose your job, which their site says at no fault of your own, SoFi has an Unemployment Protection Program. Seems though as if you quit, you would still be on the hook and not eligible for this program.

You will be able to put your loan into forbearance in 3 month increments for a max of 1 year. This is a fraction of the time you will receive compared to Federal Loans.

Your loan will continue to accrue interest during your forbearance.

To be eligible for SoFi’s unemployment protection there are a few criteria you must meet:

You can see there are far fewer options to protect you if you were to lose your job or have an economical hardship.

This is something you should keep in mind. Especially if you are in a career where the job market it is quite volatile.

JetBlue Promotion:

Now that we are beyond the protection piece, let’s take a look at this JetBlue offer.

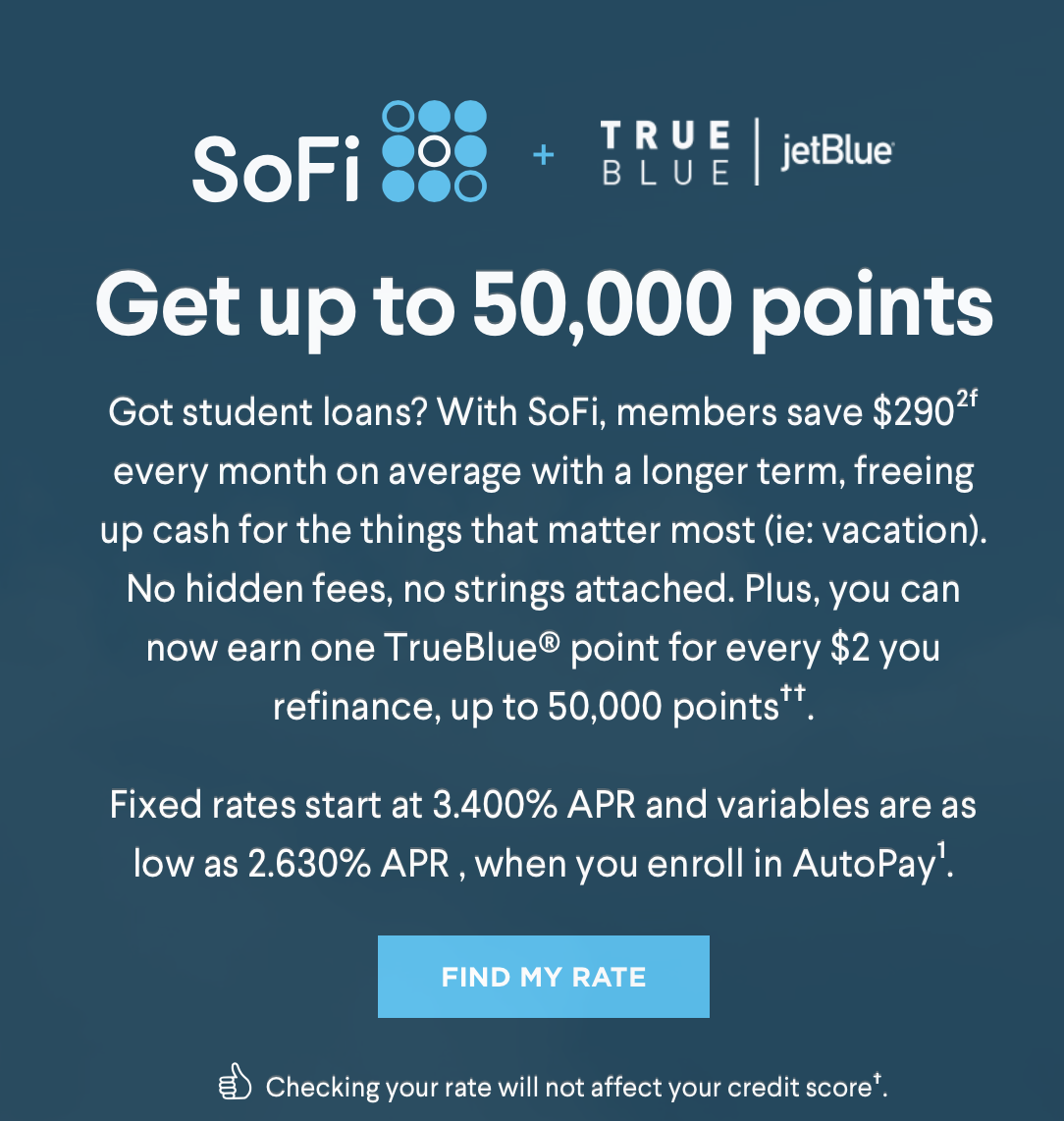

In order to earn the entire 50,000 JetBlue miles, you would need to refinance $100,000 in student loan debt. That is a lot of money, but I’m sure there are many with a 6 figure student loan balance.

The value of 50,000 JetBlue miles, is somewhere in the ballpark of $800 to $900 dollars.

I almost find it comical they offer fixed rates at 3.4%, but I’ve yet to hear of a person who has received a rate that low. When I refinanced I believe my credit score way just shy of 800 and I still didn’t qualify for their best rate.

And personally, I wouldn’t apply for a variable rate, but if you were to do that you have the possibility to have a lower interest rate. But, I wouldn’t hold your breath

To be eligible, SoFi has a few rules for you:

- You must provide your TrueBlue member number

- Complete a loan application with SoFi for student loan refinance

- Register and/or apply through the landing page of Sofi.com/jetblue

- Meet SoFi criteria

If you can meet the criteria and are approved to refinance your student loans, your points will be deposited within 90 days.

One question I have about this process and I would recommend you to explore as well. If you take advantage of this offer, will your interest rate be slightly higher than someone who doesn’t? Always worth checking for yourself.

If the answer to this is yes, then this deal is absolutely worthless. While points are great, I personally want the lowest interest rate possible, especially when it comes to a large amount of money like this.

Run The Numbers:

You should be running the numbers for many things in the credit card game to begin with. If you have a large amount of student debt this is even more important. The idea is to pay off that debt, right?

This offer is definitely not for everyone. I would really only consider this offer if:

- You planned/were on the fence to refinance your Federal Student Loans to begin with

- SoFi is the best option for you

- The interest rates are the same between the JetBlue offer and Non-JetBlue offer.

There are a lot of things to consider when looking to refinance your student loans. Don’t look at the miles only, this might cost you a lot of money in interest and if you ever did lose your job, your protection wouldn’t be ideal.

Putting It All Together:

Every person has a different situation when it comes to their student loans. Luckily, there are options to help you pay them off a little sooner or at a lower interest rate.

SoFi and other companies who offer refinancing are not for everyone. They offer fewer protections in case you lose your job, or other financial situations arise. This not only could cost you more money, since interest will be accruing, but also you’d be taking a hit on your credit score. There are many things you need to evaluate before considering refinancing your student loans.

If you are someone with $100,000 in student loan debt and were going to refinance before this offer came up. Then go for it as long as the interest rates are the best for you.

If you weren’t going to refinance to begin with, it might be best to just delete that email. While JetBlue miles are valuable, they aren’t THAT valuable.

My Experience with SoFi:

I never had an issue with SoFi. The refinancing process was very quick and the customer service was very good. They offered me the best rate I could receive at the time for refinancing my loans.

I was able to use Plastiq to meet many minimum spend requirements while paying off my student loans at the same time. I never had any issues with payments not posting to my account. Although, I have read people have had issues with payments not posting.

I would definitely recommend them for someone looking to refinance their loans, but only if they offer you the best interest rates.

Conclusion:

While 50,000 JetBlue miles is a nice chunk of points, the decision to refinance your student loans should not be made based on points. There are many protections you are losing when you move your Federal Student Loans to a private loan.

Unless you had plans to refinance, have a stable job, and SoFi offers the best interest rate to you, I would say pass on this deal.

Do you plan to refinance your student loans for 50,000 JetBlue points?

Consider Subscribing to my YouTube Channel, Follow me on Instagram, Like me on Facebook, or Follow me on Twitter. If you have questions, comments or would like a topic, leave a comment. Thank you for reading!

What about the credit score implications to refinancing? I have student loans that are 11 years old. I’ve paid them down significantly, but if I refinance them, will that account age then go to zero, and thus hurt my credit score? If so, I’d rather just continue to pay balance down, then once they are really low, stop paying until due date and milk it as long as I can.

Hey WR,

I can say my credit score did not go down when I refinanced. The amount of money I saved was worth the risk of losing a few credit points as well. Also when I paid them off, my credit went up slightly as well.

Thanks for reading! I appreciate it!

Hi Dustin, thanks for the thorough post! I’ve been looking at SoFi to consolidate my wife’s student loans and this is a helpful overview. If you don’t mind me asking, how did the interest rate you got from Sofi compare with your federal loan? I’m curious how those numbers worked out comparatively (monthly payments for example)

Hey Mike,

My interest rate was around 5.5%, which wasn’t fantastic, but it was about 2-2.25% lower than my grad plus loans. To put that into perspective of the amount of money I saved.

I was able to keep the same payment, but moved from a 10 year loan to a 5 year loan. Most of the money I put towards my loan went to principle and I was able to make plenty of principle only payments, which really helped me pay them off within 2.5ish years once I refinanced. Hope that helps.

Thanks for reading! I appreciate it!

We had $30K in student loans at 6% and 8% – one federal and one private. Like you, it was frustrating that half the minimum payment went to interest each month. We refinanced with Sofi/JetBlue about 8 months ago and were very happy with the experience as it was mostly online. I cosigned for my wife’s student loans and we both have excellent credit and we qualified for their lowest advertised fixed rate (3.25 at the time). The JetBlue points posted pretty quickly after the loan got funded. We’re currently working to pay the loans off as aggressively as possible and we’re so happy to see the majority of our payments going toward principal!

Hey Geoff,

I so wished the Jetblue option was available when I was refinancing! My wife and I would have had 100k JetBlue points! We were super aggressive as well and I can tell you, being student loan free is great.

Also, I’m jealous of that awesome interest rate you received!

Thanks for reading! I appreciate it!

Hi, in case anyone is interested there is also the same offer for alaska miles. sofi.com/alaska.

This is really helpful. I’m looking to refi wife’s loans and came across the Jetblue partnership but was trying to search for other partnerships and couldn’t find anything. Alaska miles would probably be worth more than jetblue pts would be