As the battle for new consumers grow, banks are definitely trying to be (what I’ll call) conservatively aggressive. They are rolling out a new “premium” credit cards, but they aren’t making these cards premium. The newest Bank of American credit card falls flat, and it hasn’t even been released yet. While this Bank of America card doesn’t “Wow” me, I think it actually shows us what the future could hold for credit cards.

The New Bank of America Credit Card Falls Flat

There were quite a few places I saw that were saying this card would somehow compete with the Chase Sapphire Reserve. After the details of this card were release that was quickly dismissed, because it comes no where near that realm of “premiumness.”

I would actually say this card falls more in line with Capital One Venture or the Barclay Arrival Plus, if you were looking to compare it. This is travel cash back card and there’s nothing wrong with these cards.

The Positives of the Card

As with many credit cards, our eyes always head toward the sign up bonus. It will come with a 50,000 point bonus after $3,000 spend in the first 90 days.

The Bank of America card will also have a couple of benefits, one of which puzzles me:

- $100 credit for Global Entry/TSA-Precheck. This is pretty common now, so everyone has this benefit 🙂

- $100 travel credit, which I believe is unsustainable and will be cut after it’s first year.

- There will be no foreign transaction fee

What puzzles me about the travel credit, is the fact it is greater than the annual fee of the card. I still don’t like the travel credit benefit, because I think travel credits are actually prepaying your travel. I see this benefit being reduce at some point, because I can’t see how this stays sustainable over the long term.

The Negatives of the Card

All cards have negatives, but we have to balance the positive and negatives. Maybe one day we can customize our cards to our liking and have an annual fee that correlates with that. A boy can dream, right?

There is a $95 annual fee, which I believe is not waived the first year.

The earning categories of this card aren’t anything to rave about. Earning 1.5x on all non-bonus spend is the same as 1.5 cents, but that is lower than a 2% cash back card (which should be the minimum you earn).

The bonus categories of 2x on dining and travel is the same as using a 2% cash back card. Plus it falls short to other cards with a similar annual fee, that are mid-level premium cards.

Making the Card Worth Your Time

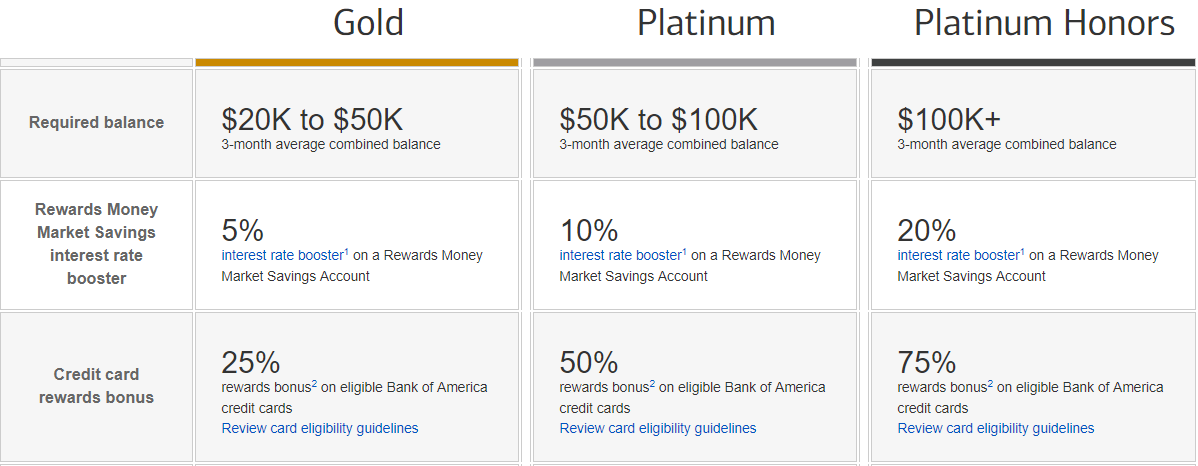

The only way I feel you could justify using this card at all, is if you are a Bank of American Platinum Honors member,or maybe a Platinum member.

In order to be a Platinum Honors member you need $100,000 in an account through Bank of America or Merrill Lynch. That is no small amount of money, but if you can hit that threshold, Bank of America credit cards become a top earner for you.

If you can hit the Platinum level, you could make the argument the card is a solid option for non-bonus spend, with an earn rate of 2.25%. There are cards now like Alliant and USAA which offer better returns at 2.5% on non-bonus spend (Alliant is 3% for year 1, then 2.5% afterwards).

The “Better” Bank of America Credit Card

I think this card will get some love, just for the 50,000 point bonus. I see nothing wrong with this new card from a bonus perspective, but when comparing to the BankAmericard Travel Rewards credit card, they are fairly similar. Except the BankAmericard comes with no annual fee, and has the same 1.5x on all non-bonus spend. To earn an extra 0.5x (or 0.75x for Platinum, or 0.88x if you are a Platinum Honors) does not seem to be worth the $95 fee.

The travel credit is nothing more than you prepaying your own travel. You still pay $95 up front for the card and are “paid back” by this card. And as I said earlier, I can’t see this benefit lasting beyond the first round of “enhancements.” I see this being cut to $50, or even being possible eliminated.

The BankAmericard Travel Rewards earns a base of 1.5 points per dollar spent and is included in Bank of America’s Preferred Program. The only “advantage” the new Bank of America card has is the 2x on all dining and travel. To me, there are better cards that earn in those categories anyway.

This is taking into account you having either Platinum or Platinum Honor status. If not, then there are better cards for you.

The Future of Credit Cards?

If Bank of America has shown us anything, they are showing us they want to reward customers who have a banking relationship with them. The more money you have with them, the better the rewards. If banks decide to head down this road, unless you have A LOT of money to mix between banks, you’ll likely have to stick with one bank.

I do think we will see credit card bonuses decrease and possible be a fraction of what we see today. I believe that this is a few years away, but I do think it will happen. It will only take 1 bank to make this movement start and others will follow.

Although, some may disagree, did you ever think an airline or hotel would completely remove an award chart? How about variable pricing based on award flights? I’m sure many, or at least some of you would say no to this. The trend is this will occur as time goes on. So, I say the idea of lower credit card bonuses are not out of the question. The trade off would be higher daily return based on banking relationship.

Banks have become tired of churners. There seems to be more restrictions on earning a bonus every couple of months. Include the fact the mainstream media has increased their coverage of these topics. The point is banks don’t like “us.”

We aren’t profitable and banks keep imposing rules to prevent bonus chasing. What banks do like are profitable customers. What better way to start enticing people to be “loyal,” than to offer extra rewards based on banking relationships?

For example, my USAA Limitless, earns 1.5% cash back as a base earning. In order to earn an extra 1%, for a total of 2.5% ,I MUST deposit $1,000 to this account monthly to keep earning the extra percentage. Since I think 2.5% is quite awesome, I will continue to meet this requirement.

Conclusion

I can understand why Bank of America wants to join in the “premium” credit card market, it’s lucrative. In order to do so, they really need to re-evaluate what they consider a premium credit card. Until they do, this falls in-line with mid level reward credit cards like the Capital One Venture or Barclay Arrival Plus.

Bank of America does reward it’s customers well, if you can meet the banking requirements. This is a great way for banks to give a better earning rate to their “more profitable” customers. I believe we will see more of this over the next year and eventually see a reduction in credit card bonuses.

Do you think this card is a “premium” card? What are your thoughts on banks rewarding customers who actually bank with them?

Don’t forget to Like me on Facebook, or Follow me on Twitter. If you have questions, comments or would like a topic, leave a comment. Thank you for reading!

Great post. I agree with pretty much everything you said, however I don’t think this strategy will be the absolute one moving forward. You’re right in that they don’t like churners and are trying to get rid of us, however I don’t think that rewarding your more “loyal”/well off customers is going to necessarily help. Blanket statement here, but I would imagine the high majority of people who have $100k+ in combines accounts, do so because they are good with their finances and very rarely pay interest on their cards. If they have a Merrill account(s) then of course BofA will make money on their trades, etc. and they will make money on merchant fees from the cards, but not on interest. Would love to see their financial data, but what about the people that are actually loyal to BofA but make less money? I obviously don’t know the answer, but are people who make $100k+ a year and don’t pay interest more valuable customers than people who make $40k a year and do? I feel if they continue on this path they would weed out the churners, but they’d also alienate the “average” person too.

Hey Brian,

Thanks! I think you raise some great points. People who make more, tend to spend more. Which means more interchange fees, etc. But, I agree they are less likely to hold a balance and banks make a killing on interest from CC debt.

I actually received an email today from SoFi, mentioning that USAA made $40.08 on each $1,000 a person had in their savings account, while only paying out $1.07. I found that interesting.

I as well don’t know the answers and don’t think all banks would have high income restrictions, but I can see them giving higher rewards for more bank products/stronger relationship. It would help reduce the churning (in theory).

Thanks for the great comment!

Dustin

“while deceasing credit card bonuses.”

The typo in your subhead is quite a freudian slip. 🙂

Hey Colleen,

Thanks for catching my typo! All fixed now :-).

Thanks for reading, I appreciate it!

Dustin

Do you have any idea if the sign up bonus is subject to the additional bonus % for relationship customers?

Hey Betsy,

From what I have read, the BankAmericard Travel Rewards does not, so I would assume this won’t either. The Cash Rewards I have read does have it for the bonus.

Thanks for reading! I appreciate it!

Dustin

I agree that the card falls flat, but why do you think the $100 travel credit is unsustainable? The card is basically the same as the BOA Travel Rewards card + 2x for Dining/Travel, and if they implement the $100 travel credit “AMEX-style”, there will likely be significant breakage among many “normal” customers who aren’t churners, and this will likely help pay for the increased Dining/Travel expenditures. If they remove the travel credit, thus making the effective annual fee $95, hardly anyone will keep the card unless they are complete idiots, since they could just downgrade to the travel rewards card and get one of the plethora of better travel/dining cards. What is unsustainable is the 50,000 point signup bonus on a -$5 annual fee card.. that is definitely going to be cut before the travel credit gets cut, for sure.

Hey Tom,

I agree completely, the bonus will be unsustainable. I can see it dropping to 30k since it will be slightly higher than the BankAmericard Travel Rewards.

If you look at even the Amex style travel credit for the PRG, the card still has a $195 fee. Leaving Amex +95 after a person uses the credit to the max.

Have a credit that is greater than the annual fee just doesn’t make sense to me and when (if, maybe) people cancel at the end of year one to avoid another annual fee. Some benefit will need to be cut.

I agree though, most will not keep this card if the fee is completely eliminated, which is why they could reduce it.

This is all speculation on my part, but I agree the bonus definitely will be cut before the annual fee. No doubt about that!

Thanks for the great comment!

Dustin

[…] The New Bank of America Credit Card Falls Flat. – The benefits aren’t that much better than other BofA cards and it’s not that much of a premium card. However, I can see other banks implementing the deposit incentives. […]

Personally I don’t think the travel credit is unsustainable simply because I believe there are enough people who aren’t like us who will get the card and then forget to use the full value of the credit.

Now the FNBO Amex with a $100 annual airline incidental fee credit for no AF? That I don’t see as sustainable