Disclosure: I receive a commission if you are approved using the links below for the American Express cards.

I have been having some questions lately as a result of recent credit card applications. They have centered around these two main questions:

- What counts as minimum spending?

- When do my bonus points post?

Let’s break these down and try to give you some answers!

Minimum Spending

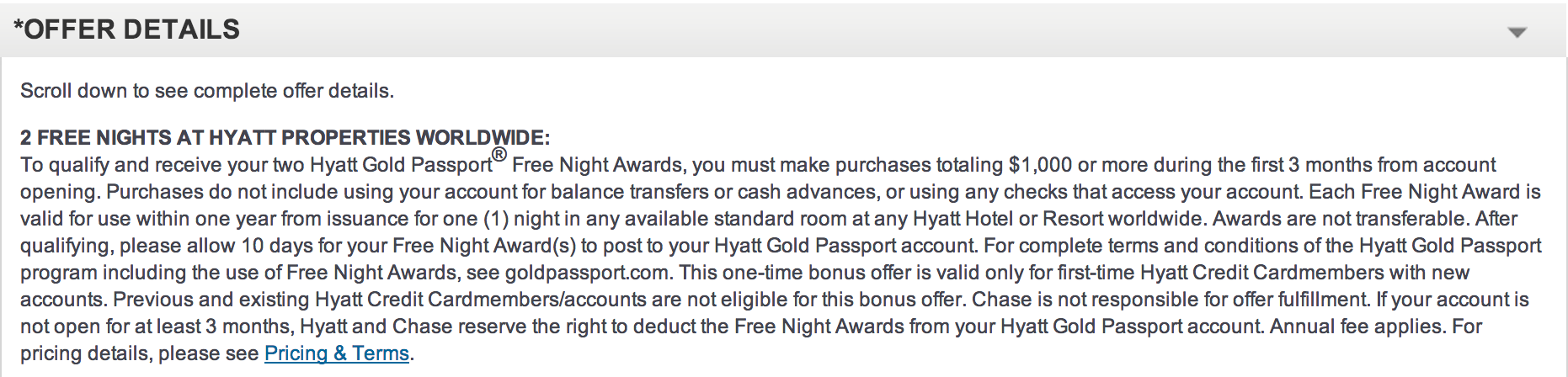

Let’s use the Chase Hyatt Visa card as our example. This card gives 2 free nights after spending $1,000 in the first three months. As with all credit card bonuses from the major banks, the minimum spending is based on purchases. Here are the terms from the card – you must make purchases totaling $1,000 or more during the first 3 months from account opening. Purchases do not include using your account for balance transfers or cash advances, or using any checks that access your account. Since that says purchases (other banks use the term eligible purchases), it means that the minimum spending must come from making actual purchases (from online sources, brick and mortar stores, Square, Paypal, Amazon Payments, etc). Annual fees, interest, balance transfer fees, convenience fees, and other card fees do not count for your minimum spending. With this card, you have a $75 annual fee up front. That $75 does not count towards your $1,000 in spending.

Here is what you need to be careful of – take note of the fees that do not count towards your minimum spending from day one! With cards such as the American Express Platinum cards, Chase United Club card, the Citi Executive AAdvantage card, or the Delta Reserve card, there are large fees slapped on the account by the close of the first billing statement. Most of those cards are over $400 fees! So, if you do not carefully track what counts as eligible spending, you might think you are $400 closer to your spending requirement than you really are. It is best if you track this on your own instead of calling to ask as the reps might not know the answer when asked.

Read those pesky terms and conditions!

When Points Post

Each bank handles the posting of points in a different way. The terms and conditions for the various cards suggest that it will take 4-8 weeks after you have met the required spending before the points post. I have never had points take the full 4-8 weeks to post, so the automated system of these banks are normally more efficient than their legal terms are. 🙂 Here is the breakdown of the major banks and my experiences with the posting of points.

- American Express – Points post within 5 days after the spending is met (if you meet the minimum spending on day one of your card, you should have the points within one week)

- Bank of America – Points post within 7 days after the spending is met (if you meet the minimum spending on day one of your card, you should have the points within 8 days)

- Barclarys Bank – Points post within 7 days after the spending is met (if you meet the minimum spending on day one of your card, you should have the points within 8 days)

- Chase Bank – Points post within 5 days after the statement that you met the spending in closes (if you meet the minimum spending on day one of your card, you should have the points within 35 days – assuming your first billing cycle is 30 days)

- Citi Banks – Points post within 3 days after the statement that you met the spending in closes (if you meet the minimum spending on day one of your card, you should have the points within 33 days – assuming your first billing cycle is 30 days)

- US Bank – Points post within 5 days after the spending is met (if you meet the minimum spending on day one of your card, you should have the points within one week)

Strategies for Making Points Post Quickly

Some of my friends are very disciplined and plan out their spending to meet the minimums within the required time on a monthly average. I am normally more impatient 🙂 and want my points right away. If you are in a position where you need your points quickly, here are some things to keep in mind that might help you with that goal.

- With Chase or Citi, you can call when you receive your card and ask them to change your closing date to an earlier date that may be more of a convenience for you. Depending on the rep, they may or may not do it.

- If you are dealing with Chase or Citi, call when you receive your card to see when the statement closes. The last thing you want (if you are needing the points to post quickly) is for the closing date to be sooner than you had thought it would be (it is not uncommon for the closing date to be 15 days after receiving your card) and just miss your required spending by the time it closes.

- If you are dealing with a card that requires something high – like $5,000 – don’t spend it all in one day at CVS or something similar! Your statement will not be closing for a few days, so spread the spending around a little. However, if you have large purchases (like airfare) obviously, go ahead and use the card for that right away. It is just the purchases that might be concerning to the bank (like 4 $1,000 purchases at a drugstore) that might cause a slight problem.

- Watch your credit limit! With cards such as the Chase Ink Bold and Chase Ink Plus, they require spending of $5,000 to get the bonus. These cards have a minimum limit of $5,000. If you received a $5,000 credit line, you do not want to max out the line the first month if you want a good, long-term relationship with the bank.

Just keep track of your spending and don’t get overzealous and you will be okay!