Well, Amex continues to march on in their quest to limit card churners (or prevent almost entirely) from getting the bonuses on cards again and again. This move was first made almost 2 years ago for personal cards but business cards had still been exempt. That has now come to an end for business cards as well.

Amex Cuts Off Churners From Business Cards With Oncer Per Lifetime Bonus Terms

Amex has cut off card churners from getting the business card bonuses

The Once Per Lifetime Bonus

In May of 2014, Amex first initiated the once per lifetime bonus terms for personal cards. Officially, it read that if you had had that product ever before, you were not eligible for the bonus again. That was a huge blow to card churners who had been used to following the previous terms, which were that you could only get the bonus if you had not had the card for 12 months. People were rotating between the business and personal cards year after year and reaping a lot of bonus miles and points. But, in 2014, personal cards became once per lifetime (or until they change that).

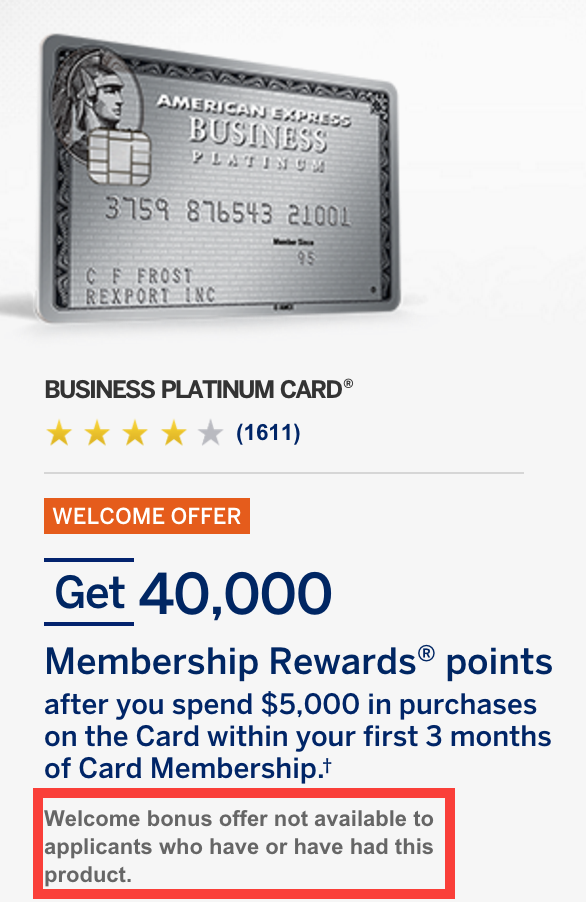

Business Cards Exempt – But Not Any More

No more repeat bonuses on Amex business cards

The good part had been that business cards were exempt and, as long as you had not had the card for 12 months, you could get the card again and again. This was great for many and something that people certainly used to their advantage. Apparently, Amex has decided that they can do without card churners on the business products as well because they finally cut that off as well. They have now instituted the same language on their business cards as they have on the personal cards. It now reads “Welcome bonus offer not available to applicants who have or have had this product.”

The good news is that their have been targeted offers sent out on the personal cards that have not had this language. This has likely been a test cast on the part of Amex to see how it works since their current policy is absolutely lousy, and not just for card churners. Hopefully, they will continue to send out targeted business card offers as well that will not include this new language. Besides, some of the best bonuses on business cards, like the Amex Business Platinum at 150K, have been targeted.

What Now?

If there are business Amex cards you have not had, make sure you wait until those cards hit their high bonus marks before you apply. Once you get it, you will not be eligible for the bonus again and they have not been good about matching offers the last couple of years. Here are some benchmarks to look for when applying for the business cards:

- Amex Business SPG – 30,000 point bonus | comes around once per year, normally at the end of summer

- Amex Business Gold Rewards – 50,000 point bonus | comes around quite often, if possible, wait for a targeted 75,000 point offer

- Amex Business Platinum – 100,000 point bonus | this one is also a targeted one and a good one to wait for, otherwise watch for a 75,000 point offer

- Amex Business Delta Gold – 50,000 miles | this normally comes around once per year

- Amex Business Delta Platinum – 50,000 award miles & 15,000 elite miles | about every 14-18 months it seems

Summary

As I have said before, I definitely do not think this is a long term, sustainable policy by Amex. They stand to lose out on a lot of return customers, not churners, that had used their products years before but would like to give them a try again. Amex cannot afford to alienate what may be great customers at this point of their business. I do think that, like Chase, this is a way for Amex to clear the deck of card churners and get a good look at the landscape before putting some more useful policy in place. I would eventually foresee them doing something like only once every 24 months on bonuses. But, for now, the business cards have been cut off for card churners and that is bad news today.

Hi Charlie,

I’m trying to meet minimum spend on American Express Business Rewards card,can I use this card to buy visa gift card and not to be charge as cash advance and secondly count as qualifying purchase to meet my $5000. spend? I would surely appreciate the help. thank you and love , love your blogs.

this will be the new standard for credit cards. one bonus per lifetime.

no more churners, anywhere.

banks make money off the churners for each transaction processed by the merchant. dont see why it is a problem for the banks…

oops. was thinking of manufactured spend. i guess the banks are in cost cutting mode.

well… it will be the new standard in the future. more will follow suit.

Gotcha!

You are right, they do make money on the spending but if the majority of churners were hitting minimums and cancelling later without another dime spent, it was a customer they got at a loss. If someone signed up through an affiliate link, the bank had paid between $100-300 for that customer already. Then, they pay about $200 or more for the bonus and are already at least $300 – $500 in the whole for the “new” customer. With transaction fees, they would need that person to spend tens of thousands and/or pay late fees and interest fees. With most churners, that does not happen.

AMEX will lose more business. I have no incentive of using their cards other than for churning… the acceptance is not universal.

I, for one, applaud this move. The churning and the associated churner (affiliate) bloggers really brought this on themselves. It might not be wrong for an indiviual to plan to churn. It is wrong for public discussions and bloggers promoting it because they get the bonus each time.

I can bet that churning would not be as prevalent if they paid affiliates only once per lifetime or if they clawed back some payment every time a cardholder dropped the card within three years.

The indiscriminate awarding of miles or points cheapened all the programs.